- Health in Perspective

- Posts

- The Dialysis Dilemma

The Dialysis Dilemma

Addressing Dialysis Cost Variation in a Fragmented System

Vinay Sudarsanam

May 14, 2025

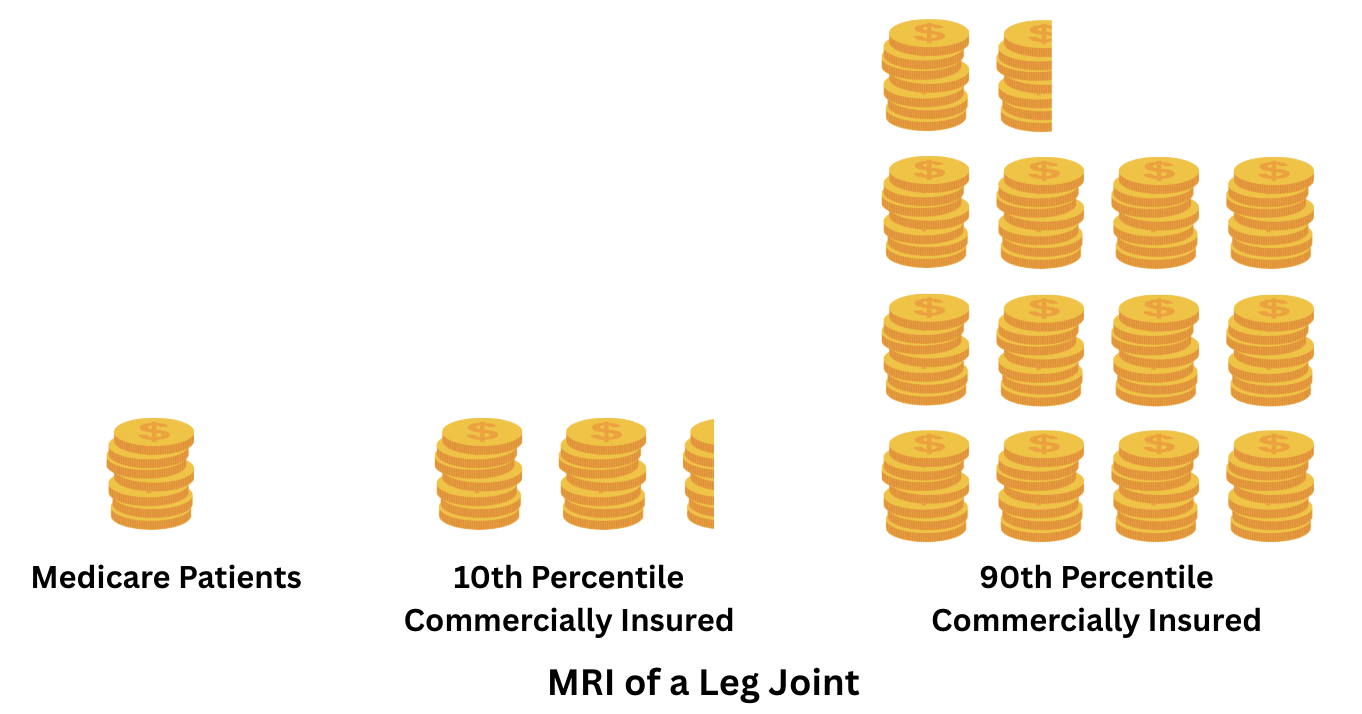

Imagine walking into a hospital for a standard MRI procedure. You pay roughly $230 whereas your friend, or another person who enters the same hospital for the same procedure, pays close to $3000. (1) How does this make sense?

I recently worked on a root cause analysis and policy brief about the “wide variation in commercial hospital prices”, a problem not unique to the U.S., but unique in its magnitude and the waste it produces in our healthcare system, with patients paying wildly different amounts for reasons unrelated to the quality or complexity of services provided. In this presentation, I stated “In the United States, two patients might pay different prices for the same healthcare service because they seek care in different states, in different metropolitan areas or cities within the same state, in different hospitals, or because those two patients are enrolled in different insurance plans.” While this seems like a very complex topic to investigate, in this post, I hope to narrow the issue’s scope to patients enrolling in dialysis clinics, and focusing on the burden of this price variation on different patient populations dealing with kidney failure. I expect this post to be the first of a multi-part series lasting for the next few months.

The U.S. healthcare system is fragmented with payers (insurers) and providers almost independently negotiating patient prices. Compared to other countries where prices for healthcare services are determined nearly entirely by government regulation, in the U.S., prices are governed more so by market forces with payers and providers leveraging their market power to affect prices at the expense of patients.

One way to think about these incentives is: hospitals might want to demand higher prices for services to compensate providers and pay for supplies used, while payers might want to demand lower prices to expand their network and insure a greater portion of the available population. However, given the diversity of payers and the fact that these payer-provider negotiations occur independently, providers end up billing patients different amounts depending on their insurer.

A larger payer that insures more people might be able to demand lower prices from hospitals as those hospitals rely on that large insured population to pay providers and for resources; on average, larger payers then have greater negotiating power to demand lower prices. The largest payer in the U.S. is the Federal Government which sets prices for public insurance programs such as Medicare, Medicaid, and CHIP amongst others. On average, these programs offer lower prices for healthcare services relative to private insurance plans.

How does this work in action? Take the example I discuss at the start of this article, about MRI costs: in North Carolina, Medicare patients might pay $228.90 for that procedure while privately insured patients might pay anywhere from $541.56 (10th percentile cost) to $3,132.68 (90th percentile cost). (1) A visual depiction of this cost variation is shown below:

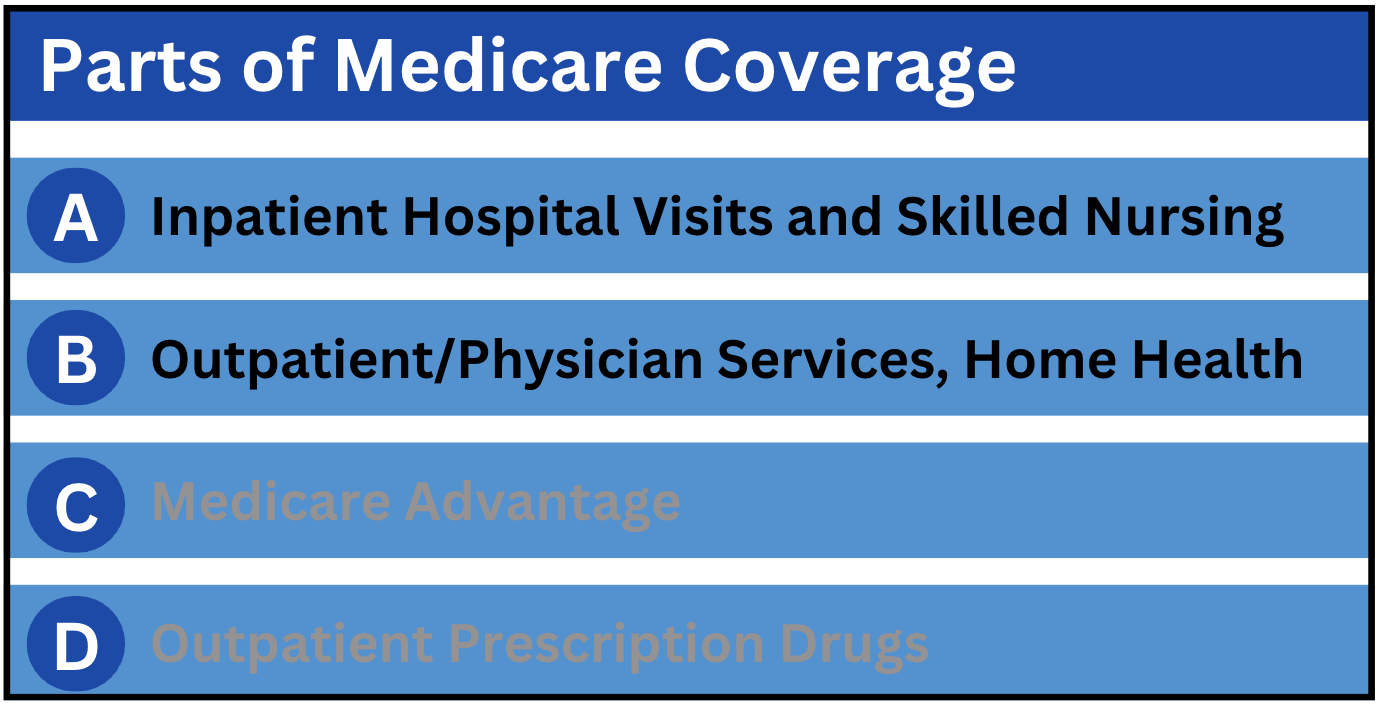

How does this apply to dialysis and kidney failure patients? Well, Medicare, a government-sponsored or public insurance program covers patients with end-stage renal disease (ESRD), and relative to the general population, costs for ESRD patients tend to be significantly higher due to the chronic nature of the disease. (2) Medicare Parts A and B cover most expenses for dialysis services; a diagram of the parts of Medicare coverage is included below:

Despite the enormity of the Medicare program, 6-7% of Medicare costs for healthcare services are for ESRD patients. (3)

So how does Medicare enrollment work for this special patient population? After a 3 month waiting period, ESRD patients become eligible for Medicare coverage and may opt for Medicare instead of their current insurance option. (2) However, after this waiting period, Medicare is a secondary insurance option to the patient’s previous (usually private) insurance plan. (3) An ESRD patient must undergo a 30 month coordination period until Medicare becomes the primary insurance option. (2) While Medicare is a secondary option, Medicare only covers what the primary insurance plan does not; namely, cost-sharing supports. (3)

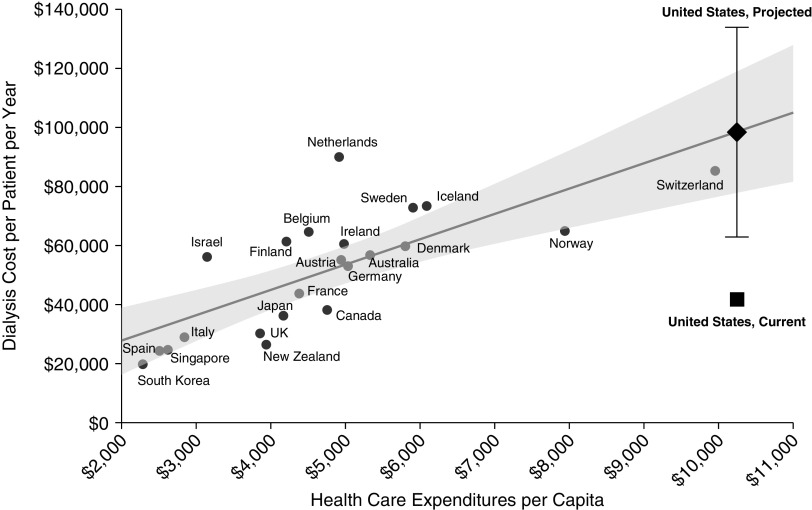

The ESRD model in the U.S. is a small example of a single-payer model, devoid of most independent payer-provider price negotiations with the federal government being the almost-universal payer. (4) While I have discussed how healthcare prices in the U.S. are on average significantly higher than those in other comparable nations, this model seemingly lacks the many inefficiencies that contribute to this trend. Using an international linear model comparing dialysis costs and health expenditures per capita, the U.S. appears significantly below its projected level, with dialysis costs per patient per year about $40,000 less than the projected amount. (4) Furthermore, dialysis costs per patient per year in the U.S. are lower than in many comparable countries including Switzerland, Norway, and Sweden, as depicted in the model below. (4)

Regardless of expected costs, let’s go back to the start of this post; significant cost disparities exist between Medicare and privately-insured patients. (2) Annual medical expenditures for Medicare patients on dialysis were roughly $80,509, significantly lower than $238,126 for those privately-insured. (2) Furthermore, for privately-insured patients with insurance from their employers (employer-sponsored), starting dialysis resulted in average monthly expenditures increasing by about 300% from $5,025 prior to dialysis to $19,710 after. (2)

Data from 2007 suggests that monthly spending for dialysis patients who are privately insured is twice as much as for dialysis patients insured by Medicare. (2) However, over the past several years, the number of dialysis patients on private insurance plans has increased (from 4.1% in 2005 to 33.9% in 2016). (5)

So what are some possible solutions to this dilemma? While privately-insured patients represent only a small share of dialysis clinic patient populations, they represent a significant share of total provider revenue. (3) Data from a single provider shows that while only 11% of patients were privately-insured, they represented about 33% of total revenue. (3) In the next few articles, I hope to discuss the current state of Medicare and private insurance options as they relate to ESRD patients, contributing to access and outcome differences between patient populations. Addressing this variation in dialysis prices is critical to reducing waste in our healthcare system and improving health outcomes for a patient population that depends on consistent, affordable care to survive.